Decaffeinated Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

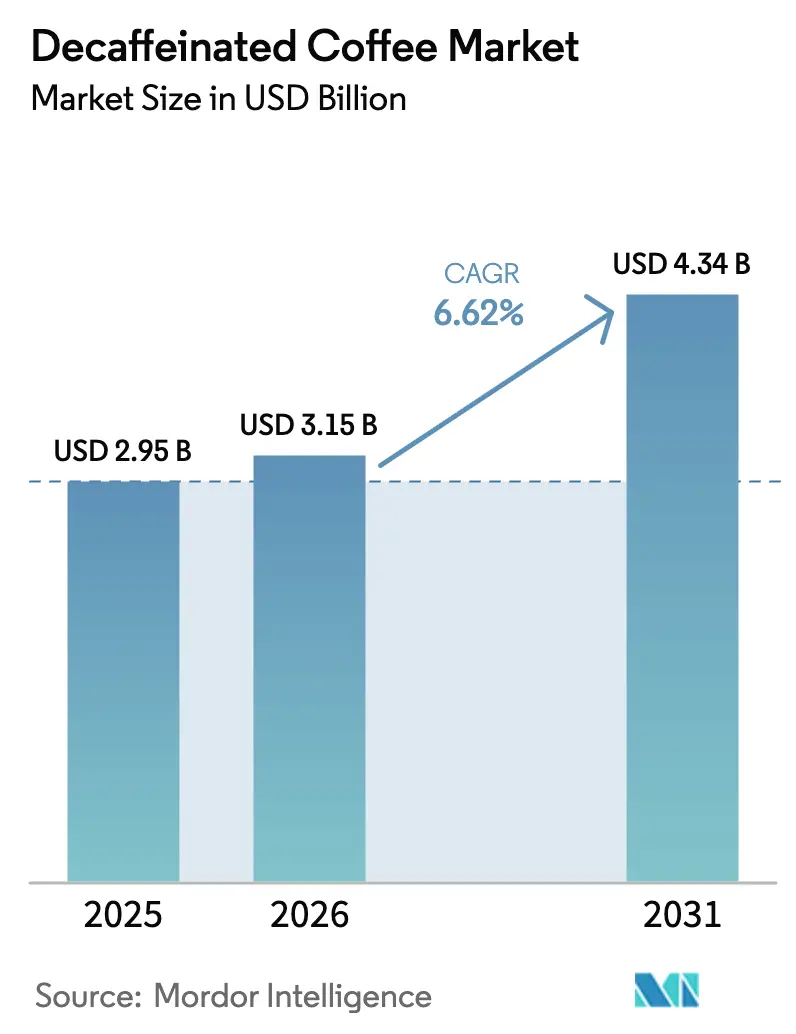

| Market Size (2026) | USD 3.15 Billion |

| Market Size (2031) | USD 4.34 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

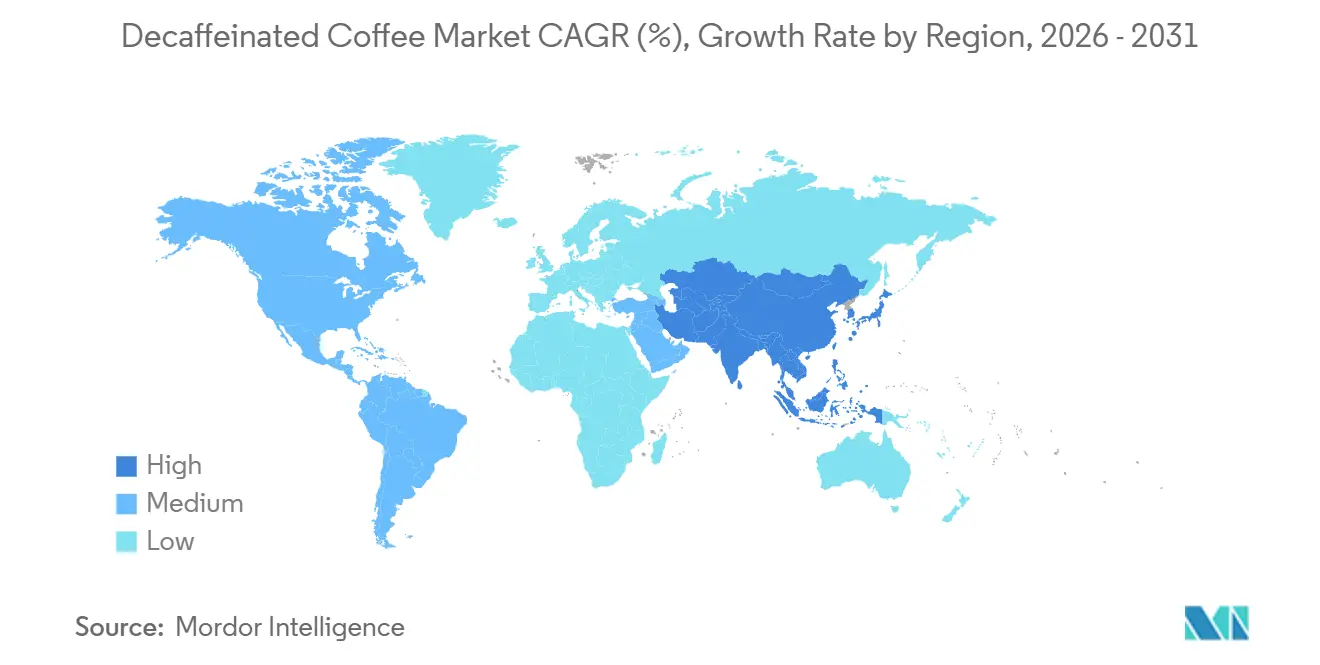

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

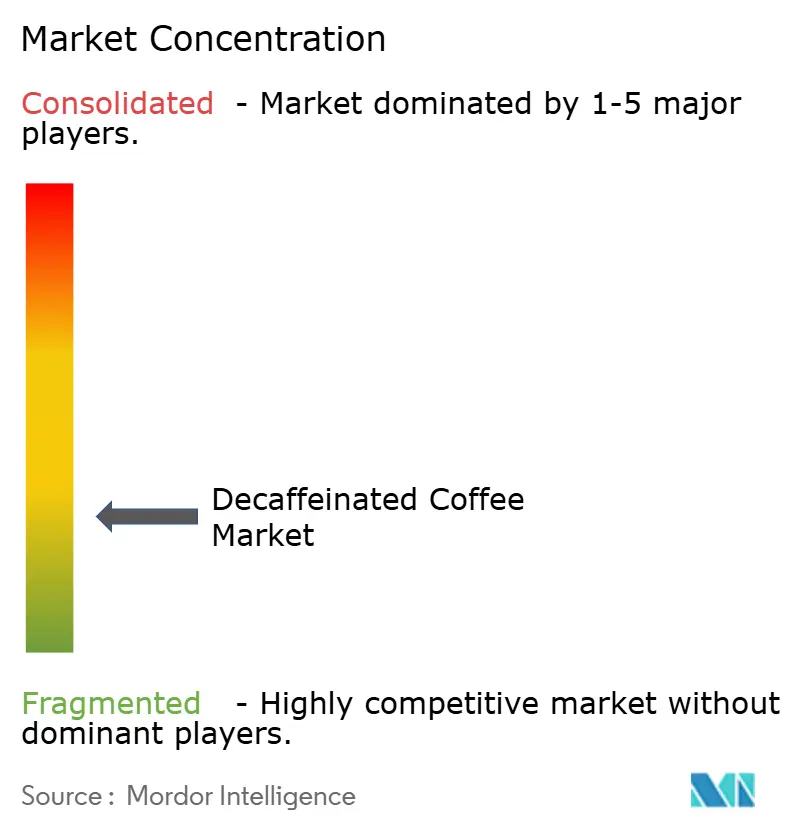

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Decaffeinated Coffee Market Analysis by Mordor Intelligence

The decaffienated coffee market size is expected to grow from USD 2.95 billion in 2025 to USD 3.15 billion in 2026 and is forecast to reach USD 4.34 billion by 2031 at 6.62% CAGR over 2026-2031. Driven by a demand for chemical-free processing and a premium positioning in specialty retail channels, health-conscious consumers are increasingly opting for decaffeinated coffee. Millennials and Gen Z now view decaf coffee as a wellness choice rather than a compromise, with many willing to pay a premium for organic or Swiss Water-processed varieties. Europe, boasting stringent quality standards and a sophisticated café culture, leads the market. In contrast, the Asia-Pacific region is witnessing the fastest growth, fueled by rising urban incomes and enhanced access to e-commerce. Technological advancements, such as subcritical CO₂ extraction, which can remove up to 99.9% of caffeine while preserving aroma, have addressed previous taste concerns, enhancing the appeal of decaf. In this fragmented market, niche roasters are carving a niche by offering origin-specific decaf options tailored to discerning tastes.

Key Report Takeaways

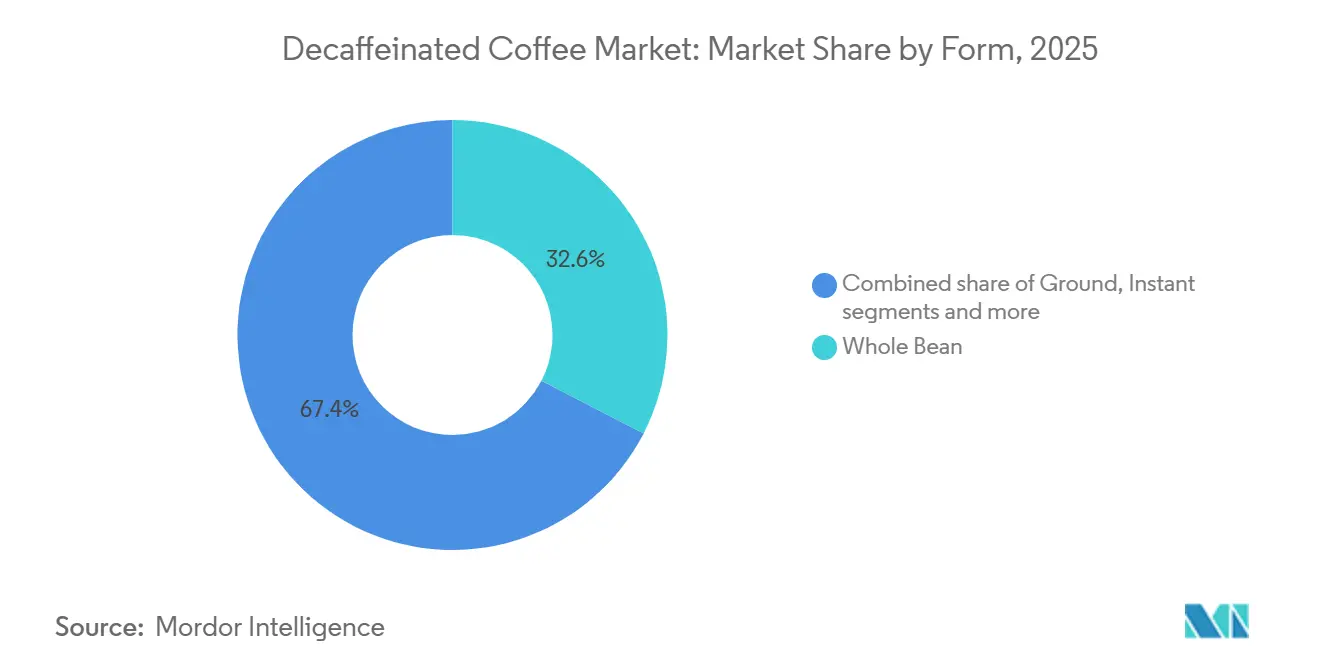

- By form, whole-bean captured 32.57% of the decaffeinated coffee market share in 2025, whereas instant is forecast to expand at a 7.24% CAGR to 2031.

- By coffee bean type, arabica led with 59.32% revenue share in 2025, while robusta is projected to grow at a 6.57% CAGR through 2031.

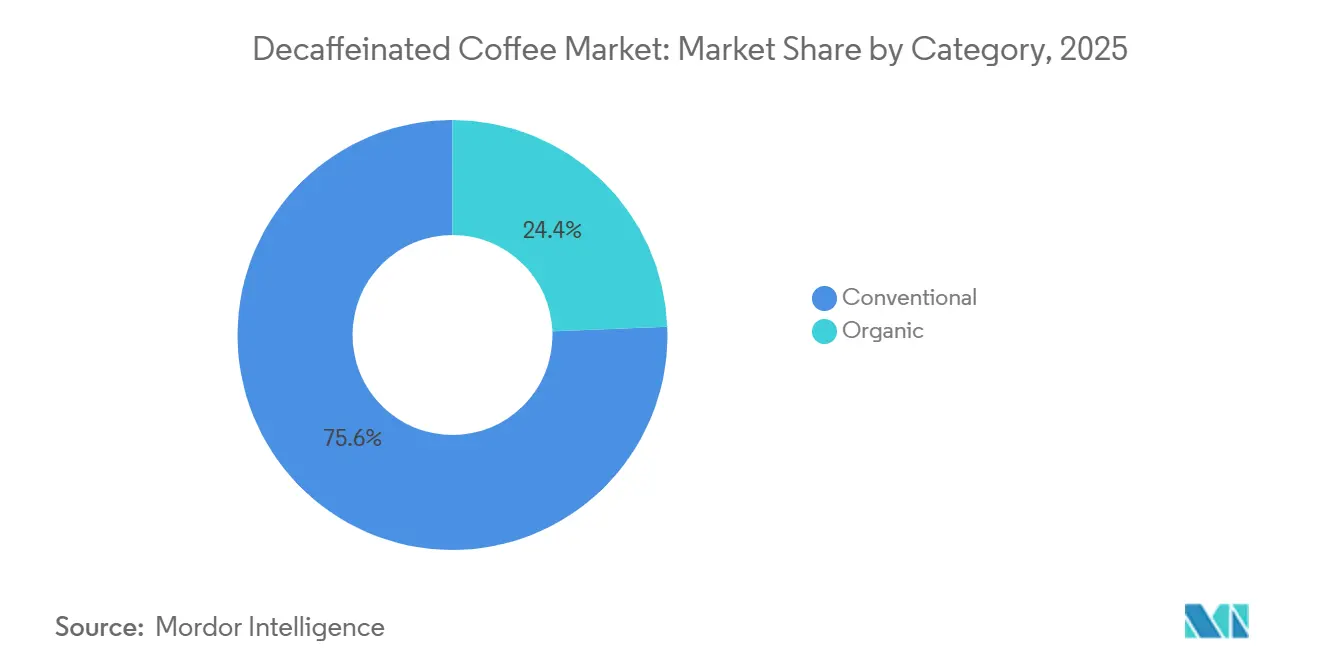

- By category, conventional held 75.61% share of the decaffeinated coffee market size in 2025; organic is accelerating at an 8.11% CAGR to 2031.

- By decaffeination method, solvent-based retained 39.75% share in 2025, whereas swiss water Process is advancing at an 8.16% CAGR over 2026-2031.

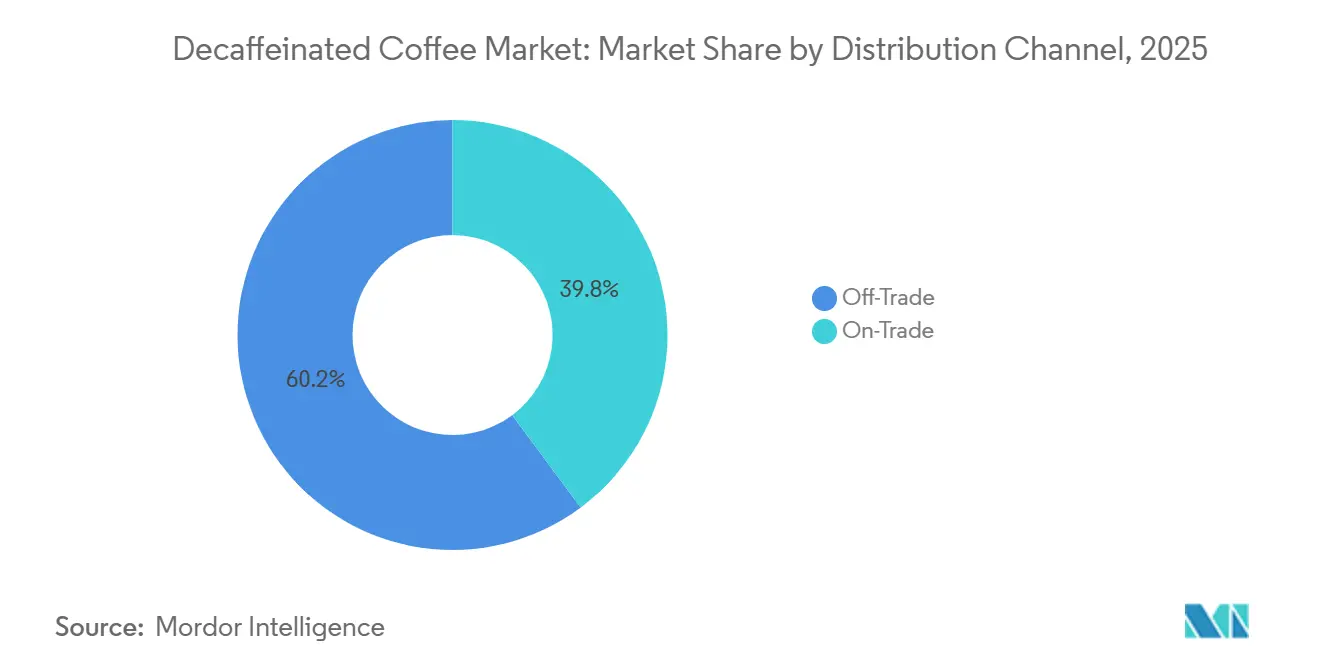

- By distribution channel, off-trade dominated with a 60.17% share in 2025, while on-trade is poised to grow at a 7.13% CAGR through 2031.

- By geography, Europe accounted for 39.76% of 2025 revenue; Asia-Pacific is the fastest-growing region at a 6.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Decaffeinated Coffee Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health awareness and preference for low-caffeine beverages | +1.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Growing preference among millennials and Gen Z for specialty decaf options | +1.5% | North America, Europe, urban Asia-Pacific (China tier-1 cities, Japan, Australia) | Short term (≤ 2 years) |

| Growing aging population seeking reduced caffeine intake | +0.8% | Europe, North America, Japan | Long term (≥ 4 years) |

| Expansion of premium, organic, and specialty decaf coffee offerings | +1.3% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Rising demand for clean-label and chemical-free decaffeination processes | +1.4% | North America, Europe, Australia, early adoption in urban Asia-Pacific | Short term (≤ 2 years) |

| Growth of café culture and out-of-home coffee consumption | +1.1% | Global, with spillover from Europe and North America to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health awareness and preference for low-caffeine beverages

Increasing health consciousness and the demand for low-caffeine beverages are key drivers of growth in the decaffeinated coffee market, as more consumers aim to enjoy coffee without the adverse effects of caffeine. The 2025 Lavazza consumer survey indicates that 62% of Brits avoid drinking regular coffee in the afternoon due to concerns about caffeine, while 44.7% now consume decaf at home, a notable rise from almost negligible levels ten years ago[1]Source: Lavazza, “The 2026 Lavazza Calendar”, lavazza.com. This shift reflects a broader trend toward wellness, better sleep, and mindful consumption habits. In response, both specialty coffee brands and mainstream retailers are expanding their decaffeinated portfolios across multiple formats, from whole beans and ground coffee to instant and ready-to-drink options. Advanced decaffeination techniques that maintain flavor integrity while reducing caffeine content have made decaf products more appealing to a wider audience. Consumers are increasingly viewing decaffeinated coffee not merely as a substitute but as a health-conscious alternative. With growing awareness of caffeine-related concerns, the segment is poised for continued adoption and steady market expansion.

Growing preference among millennials and Gen Z for specialty decaf options

The growing preference among millennials and Gen Z for specialty decaffeinated coffee is emerging as a significant driver in the market, fueled by a combination of social media influence and increased coffee education. Many young consumers showcase premium decaf as part of a mindful, health-conscious lifestyle, elevating its perception beyond a simple caffeine alternative. According to the National Coffee Association, specialty coffee consumption in the U.S. has risen 18% since 2020, reaching 46% of adults by January 2025, with younger demographics accounting for much of this growth[2]Source: Lavazza, “The 2026 Lavazza Calendar”, lavazza.com. This trend indicates that younger consumers are not only exploring flavor, origin, and brewing methods but also incorporating decaf as part of broader lifestyle choices. Coffee brands are responding by offering premium decaffeinated blends, single-origin options, and innovative brewing formats that cater to this audience. As a result, the millennial and Gen Z focus on specialty decaf is expanding the market and creating new opportunities for product differentiation and engagement.

Growing aging population seeking reduced caffeine intake

The growing aging population is increasingly driving demand for decaffeinated coffee, as older consumers often seek to reduce caffeine intake due to health considerations such as hypertension, heart conditions, and sleep sensitivity. Many in this demographic continue to enjoy the ritual and taste of coffee but prefer options that do not interfere with their wellness routines. Decaffeinated coffee allows them to maintain regular consumption without the stimulating effects of caffeine, making it a suitable lifestyle choice. Health awareness campaigns and education on the benefits of low-caffeine diets have further encouraged adoption among older adults. Coffee brands are responding by offering milder, smooth-flavored decaf options and convenient formats such as instant or single-serve pods, catering to both taste and ease of preparation. Additionally, the combination of premiumization and improved decaffeination processes ensures flavor retention, which appeals to this discerning consumer group.

Expansion of premium, organic, and specialty decaf coffee offerings

The expansion of premium, organic, and specialty decaffeinated coffee offerings is a key driver propelling the market, as consumers increasingly seek high-quality, health-conscious, and ethically sourced options. Brands are introducing single-origin decaf, artisanal blends, and organic-certified products to cater to the growing demand for superior taste and sustainable practices. This trend is particularly pronounced among urban, health-conscious, and younger consumers who value transparency, flavor complexity, and eco-friendly sourcing. Retailers and specialty cafés are promoting these offerings through curated selections, highlighting certifications such as organic, Fair Trade, and chemical-free decaffeination methods. The premiumization of decaf also allows brands to differentiate themselves in a competitive market and command higher price points. Advanced decaffeination techniques, including Swiss Water and CO₂ processes, ensure that flavor integrity is maintained, appealing to discerning coffee drinkers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production cost of decaf beans versus regular coffee | -1.0% | Global, acute in regions with volatile Arabica futures (South America, East Africa) | Short term (≤ 2 years) |

| Persistent perception of inferior taste and aroma | -0.7% | Global, particularly in developing markets with limited specialty coffee exposure | Medium term (2-4 years) |

| Limited awareness and availability in developing regions | -0.5% | Asia-Pacific (excluding Japan, Australia), Middle East, Africa, South America (excluding Brazil) | Long term (≥ 4 years) |

| Supply chain complexity and dependency on specialized processing facilities | -0.4% | Global, with concentration risk in North America and Europe processing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher production cost of decaf beans versus regular coffee

The elevated production cost of decaffeinated coffee beans compared to regular coffee remains a significant market constraint. Decaffeination requires additional processing steps such as Swiss Water, CO₂, or solvent-based methods which involve specialized equipment, longer processing times, and increased labor and energy requirements. These added expenses often translate into higher retail prices, making decaf less accessible to price-sensitive consumers. Sourcing premium green beans suitable for decaffeination, particularly for organic or specialty varieties, further increases production costs. Smaller producers face difficulties achieving economies of scale, which can limit their competitiveness. Consequently, higher prices can deter frequent purchases, especially in markets where regular coffee is more affordable. While consumer demand for decaf is growing due to health and lifestyle trends, the cost-intensive nature of production continues to restrict widespread adoption and market expansion.

Persistent perception of inferior taste and aroma

The decaffeinated coffee market faces a significant restraint due to the persistent perception that decaf offers inferior taste and aroma compared to regular coffee. Lavazza reports that, in 2024, 46% of UK respondents believe decaf coffee tastes worse, and 32% view it as inherently inferior. These perceptions highlight a skepticism about decaf quality, even with technological advancements. Bridging this perception gap will demand ongoing marketing efforts[3]Source: National Coffee Association, "National Coffee Data Trends 2025", www.ncausa.org.. This view stems from earlier decaffeination methods, which often removed essential flavor compounds and left beans with a flat or slightly bitter profile. Despite improvements through modern techniques like Swiss Water and CO₂ processes, many consumers still associate decaf with a less satisfying coffee experience. Such perceptions can discourage trial and reduce repeat purchases, particularly among specialty coffee drinkers who prioritize flavor complexity. Overcoming this bias requires targeted marketing, education, and promotion of high-quality decaf options. Premium decaf blends, single-origin offerings, and chemical-free decaffeination methods are increasingly being used to shift consumer attitudes.

Segment Analysis

By Form: Whole-Bean Premiums Offset Instant Convenience Gains

Whole-bean decaffeinated coffee accounted for the largest share of the market in 2025, capturing 32.57% of total revenue, reflecting strong consumer preference for freshness, aroma, and a more authentic brewing experience. This segment continues to benefit from the growing popularity of home brewing methods such as French press, pour-over, and espresso machines, where whole beans are perceived to deliver superior flavor quality. Additionally, specialty coffee culture has played a significant role in driving demand, as consumers increasingly seek premium and artisanal coffee experiences even in decaffeinated variants. The ability to grind beans to a preferred consistency also provides greater control over taste and strength, further supporting its widespread adoption. Retailers and coffee brands have responded by expanding their portfolios with high-quality, single-origin, and organic decaffeinated whole-bean offerings.

In contrast, the instant decaffeinated coffee segment is projected to be the fastest-growing category, expanding at a CAGR of 7.24% through 2031, driven primarily by convenience and time-saving attributes. Increasingly busy lifestyles and the growing need for quick, hassle-free beverage options are key factors propelling demand for instant formats. This segment is also gaining traction among younger consumers and urban populations who prioritize ease of preparation without compromising significantly on taste. Manufacturers are investing in product innovation to improve flavor profiles, aroma retention, and solubility, helping to reduce the traditional quality gap between instant and brewed coffee. Additionally, the rise of on-the-go consumption and travel-friendly packaging formats has further strengthened the appeal of instant decaffeinated coffee.

Note: Segment shares of all individual segments available upon report purchase

By Coffee Bean Type: Arabica Dominance Faces Robusta Processing Gains

Arabica beans accounted for the largest share of the decaffeinated coffee market in 2025, contributing 59.32% of total revenue, driven by their superior flavor profile, mild acidity, and aromatic complexity. Consumers generally associate Arabica with premium quality, making it the preferred choice for both at-home brewing and specialty coffee consumption. The segment has benefited significantly from the expansion of specialty coffee culture, where taste differentiation and origin-specific characteristics are highly valued. In the decaffeinated segment, maintaining flavor integrity is particularly important, and Arabica beans are better suited to retain nuanced taste notes even after the decaffeination process. Additionally, increasing demand for organic, single-origin, and sustainably sourced coffee has further strengthened the dominance of Arabica in the market.

In contrast, Robusta beans are projected to be the fastest-growing segment, expanding at a CAGR of 6.57% through 2031, primarily due to their cost-effectiveness and higher caffeine content prior to decaffeination. Although traditionally considered lower in flavor complexity compared to Arabica, Robusta is gaining traction as manufacturers improve processing techniques to enhance taste and reduce bitterness. The segment is particularly appealing in price-sensitive markets, where affordability plays a critical role in purchasing decisions. Additionally, Robusta’s stronger body and bold flavor make it suitable for instant coffee formulations, which aligns with the growing demand for convenient coffee formats. Increasing use of Robusta in blends is also contributing to its growth, as it helps balance cost while maintaining acceptable taste profiles.

By Category: Organic Segment Capitalizes on Sustainability Trends

The conventional category dominated the decaffeinated coffee market in 2025, accounting for 75.61% of total revenue, primarily due to its widespread availability and cost competitiveness. Conventional decaffeinated coffee remains the preferred choice for a large base of consumers who prioritize affordability and accessibility over niche attributes such as organic certification. The segment benefits from well-established supply chains and large-scale production, enabling manufacturers to maintain consistent pricing and broad distribution across supermarkets, convenience stores, and online platforms. Additionally, major coffee brands predominantly offer conventional variants, ensuring strong visibility and consumer familiarity in both developed and emerging markets. The ease of sourcing conventionally grown coffee beans further supports high production volumes, making it the backbone of the overall market.

In contrast, the organic category is emerging as the fastest-growing segment, projected to expand at a CAGR of 8.11% through 2031, driven by rising consumer awareness around health, sustainability, and environmental impact. Consumers are increasingly seeking products free from synthetic pesticides, fertilizers, and chemical additives, which is boosting demand for organically certified decaffeinated coffee. This trend is particularly strong among health-conscious and environmentally aware consumers, especially in developed regions. Manufacturers are responding by expanding their organic product portfolios and investing in certifications to build trust and transparency. Additionally, the growth of specialty coffee culture has further accelerated interest in organic offerings, as consumers associate them with higher quality and ethical sourcing practices.

By Decaffeination Method: Swiss Water Process Challenges Solvent-Based Dominance

The solvent-based method dominated the decaffeinated coffee market in 2025, accounting for 39.75% of total revenue, largely due to its cost efficiency and widespread industrial adoption. This method, which typically uses solvents such as ethyl acetate or methylene chloride, is highly effective in removing caffeine while maintaining acceptable flavor characteristics. Its scalability and relatively lower production costs make it the preferred choice for mass-market coffee manufacturers, enabling competitive pricing across retail channels. Additionally, solvent-based decaffeination is extensively used in both instant and ground coffee formats, further strengthening its market presence. The method’s long-standing commercial use and established processing infrastructure contribute to its reliability and consistent output quality. While there are some consumer concerns regarding chemical usage, regulatory standards ensure that residual solvent levels remain within safe limits, maintaining consumer confidence.

In contrast, the Swiss Water Process is emerging as the fastest-growing decaffeination method, projected to expand at a CAGR of 8.16% during 2026–2031, driven by increasing consumer preference for chemical-free and environmentally friendly processing techniques. This method uses only water, temperature, and time to remove caffeine, preserving much of the coffee’s original flavor profile without the use of synthetic solvents. Growing health consciousness and demand for clean-label products are key factors accelerating its adoption, particularly among premium and specialty coffee consumers. The Swiss Water Process is also gaining traction in organic and sustainably certified coffee segments, aligning with broader industry trends toward transparency and eco-friendly practices. Although it is generally more expensive than conventional methods, consumers are increasingly willing to pay a premium for perceived health and quality benefits.

By Distribution Channel: On-Trade Momentum Builds Despite Off-Trade Dominance

The off-trade channel dominated the decaffeinated coffee market in 2025, accounting for 60.17% of total revenue, driven by the strong presence of retail formats such as supermarkets, hypermarkets, specialty stores, and e-commerce platforms. This channel benefits from high consumer preference for at-home consumption, where decaffeinated coffee is purchased for daily use and convenience. The wide availability of diverse product formats including whole beans, ground coffee, and instant variants further supports growth in off-trade channels. Additionally, competitive pricing, promotional offers, and bulk purchasing options available in retail environments encourage higher sales volumes. The rapid expansion of online retail has also strengthened this segment, enabling consumers to access a broad range of domestic and international brands with ease.

In contrast, the on-trade channel is projected to be the fastest-growing segment, expanding at a CAGR of 7.13% through 2031, fueled by the recovery and expansion of foodservice establishments such as cafés, restaurants, and hotels. Increasing consumer preference for out-of-home coffee experiences, particularly in urban areas, is a key factor driving growth in this segment. Specialty coffee shops are increasingly incorporating decaffeinated options into their menus to cater to health-conscious consumers and those seeking reduced caffeine intake without compromising on taste. Additionally, the premiumization trend in the coffee industry is encouraging on-trade operators to offer high-quality decaffeinated beverages, including espresso-based drinks and specialty brews. The growth of café culture, especially among younger demographics, further supports rising demand in this channel.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe held the largest share of the decaffeinated coffee market in 2025, accounting for 39.76% of total revenue, driven by a well-established coffee culture and strong consumer awareness of decaffeinated options. The region benefits from a mature market where consumers are increasingly seeking healthier alternatives without compromising on taste and quality. High consumption levels in countries such as Germany, France, Italy, and the UK continue to support steady demand for decaffeinated coffee across multiple formats. Additionally, the presence of leading global coffee brands and specialty roasters has strengthened product availability and innovation within the region. Growing interest in premium, organic, and sustainably sourced coffee further reinforces Europe’s leadership in the market. Retail infrastructure, including supermarkets and online platforms, ensures widespread accessibility of decaffeinated products.

Asia-Pacific is projected to be the fastest-growing region in the decaffeinated coffee market, expanding at a CAGR of 6.45% through 2031, driven by changing lifestyles and increasing urbanization. Rising disposable incomes and the growing influence of Western coffee culture are encouraging consumers to adopt coffee consumption, including decaffeinated variants. Markets such as China, Japan, South Korea, and India are witnessing a surge in café culture and specialty coffee outlets, which is contributing to greater product awareness. Additionally, younger consumers in the region are increasingly experimenting with different coffee types, including low-caffeine and functional beverages. The expansion of international coffee chains and e-commerce platforms is also improving accessibility to decaffeinated products.

Other regions, including North America, the Middle East and Africa, and South America, also play important roles in the decaffeinated coffee market with varying growth dynamics. North America represents a significant and mature market, driven by high coffee consumption rates in the United States and Canada, along with strong demand for specialty and premium decaffeinated products. The Middle East and Africa region is gradually emerging, supported by urbanization, increasing café culture, and a growing young population, although overall consumption remains comparatively lower. South America, being a major coffee-producing region, shows steady demand growth, particularly in countries like Brazil and Colombia, where domestic consumption is rising alongside exports. These regions are also witnessing increasing product diversification, including instant and ready-to-drink decaffeinated formats.

Competitive Landscape

The decaffeinated coffee market exhibits moderate fragmentation, characterized by the presence of several global players alongside numerous regional and niche brands. Large multinational companies maintain a strong foothold through extensive product portfolios, established supply chains, and significant brand recognition. At the same time, smaller specialty coffee roasters and emerging brands contribute to market diversity by offering differentiated products, including organic, single-origin, and sustainably sourced decaffeinated coffee. This mix of players creates a competitive environment where both scale and specialization play important roles. While global companies dominate mass-market segments, niche players are increasingly capturing attention in premium categories. The fragmented nature of the market encourages continuous innovation and competitive pricing strategies.

Competition in the decaffeinated coffee market is largely driven by product quality, decaffeination methods, branding, and distribution reach. Leading companies are investing in advanced decaffeination technologies, such as Swiss Water and CO₂ processes, to enhance flavor retention and appeal to health-conscious consumers. In addition, branding strategies emphasizing clean-label, chemical-free processing, and sustainability certifications are becoming key differentiators. Companies are also expanding their presence across both off-trade and on-trade channels to maximize market penetration. Strategic collaborations with cafés, retailers, and e-commerce platforms further strengthen competitive positioning.

Furthermore, the market is witnessing increased activity in terms of product launches, partnerships, and geographic expansion as companies seek to strengthen their competitive edge. Brands are introducing innovative formats such as ready-to-drink decaffeinated beverages and specialty blends to cater to evolving consumer preferences. Mergers and acquisitions, as well as partnerships with local distributors, are enabling companies to expand into emerging markets and enhance their regional presence. Sustainability initiatives, including eco-friendly packaging and ethically sourced beans, are also becoming central to competitive strategies. Additionally, digital marketing and direct-to-consumer channels are playing a growing role in brand building and customer engagement.

Decaffeinated Coffee Industry Leaders

-

Nestlé S.A.

-

JDE Peet’s N.V.

-

The Kraft Heinz Company

-

Starbucks Corporation

-

The J.M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Nespresso introduced a limited-edition Vertuo pod, Decaf Lavender & Vanilla Flavour. This pod, crafted from 100% Arabica beans using the Swiss Water method, was aimed at consumers who perceived decaf as an exploration of flavors rather than merely a caffeine-free choice. This launch underscored Nestlé's ambition to elevate the decaf segment, blending transparent sourcing with unique flavor innovations.

- June 2025: Lavazza North America launched Dolcevita Decaf, a premium decaffeinated coffee catering to the growing demand for high-quality, caffeine-free options. Part of the Dolcevita range, the medium roast blend features a full-bodied flavor with chocolate and caramel notes. Available at select retailers and online, the launch highlights Lavazza's focus on innovation and customer feedback.

- May 2025: New online brand Dekáf Coffee Roasters, specializing in premium decaf, has debuted with offerings that are both small-batch and sustainably sourced. Prioritizing flavor, it ensures fresh deliveries to its discerning coffee aficionados.

- April 2025: Free Rein Coffee Company unveiled its first decaf offering, named Spurless. This bold dark roast, made from 100% Arabica beans, was designed to provide a rich and robust flavor experience while being caffeine-free. The launch marked a significant step for the company as it expanded its product portfolio to cater to the growing demand for high-quality decaf coffee options.

Global Decaffeinated Coffee Market Report Scope

Decaffeinated coffee is a type of coffee from which most of the caffeine has been removed while retaining the original flavor, aroma, and characteristics of the coffee beans. The decaffienated coffee market is segmented by form, coffee bean type, category, decaffienation method, distribution channel and geography. Based on form, the market is segmented into whole-bean, ground, instant and others. By coffee bean type, the market is segmented into arabica, robusta and others. By category, the market is segmented into conventional and organic, By decaffeination method, the market is segmented into solvent-based, swiss water process, supercritical co₂ and triglyceride process. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Whole Bean |

| Ground |

| Instant |

| Others |

| Arabica |

| Robusta |

| Others |

| Conventional |

| Organic |

| Solvent-Based |

| Swiss Water Process |

| Supercritical CO₂ |

| Triglyceride Process |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Form | Whole Bean | |

| Ground | ||

| Instant | ||

| Others | ||

| By Coffee Bean Type | Arabica | |

| Robusta | ||

| Others | ||

| By Category | Conventional | |

| Organic | ||

| By Decaffeination Method | Solvent-Based | |

| Swiss Water Process | ||

| Supercritical CO₂ | ||

| Triglyceride Process | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the decaffeinated coffee market in 2031?

It is forecast to reach USD 4.34 billion by 2031 at a 6.62% CAGR.

Which decaffeination method is growing fastest?

Swiss Water Process leads with an expected 8.16% CAGR over 2026-2031 due to clean-label demand.

Which region shows the highest growth potential for decaf coffee?

Asia-Pacific is set to expand at 6.45% CAGR, driven by café culture penetration in China and India.

How big is organic decaf compared with conventional products?

Organic accounted for less than one-quarter of 2025 sales but is growing at 8.11% CAGR, outpacing conventional.

What share did Whole-Bean formats hold in 2025?

Whole-Bean captured 32.57% of global revenue, reflecting consumer appetite for premium taste.