Tappet Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 9.79 Billion |

| Market Size (2031) | USD 11.34 Billion |

| Growth Rate (2026 - 2031) | 2.97% CAGR |

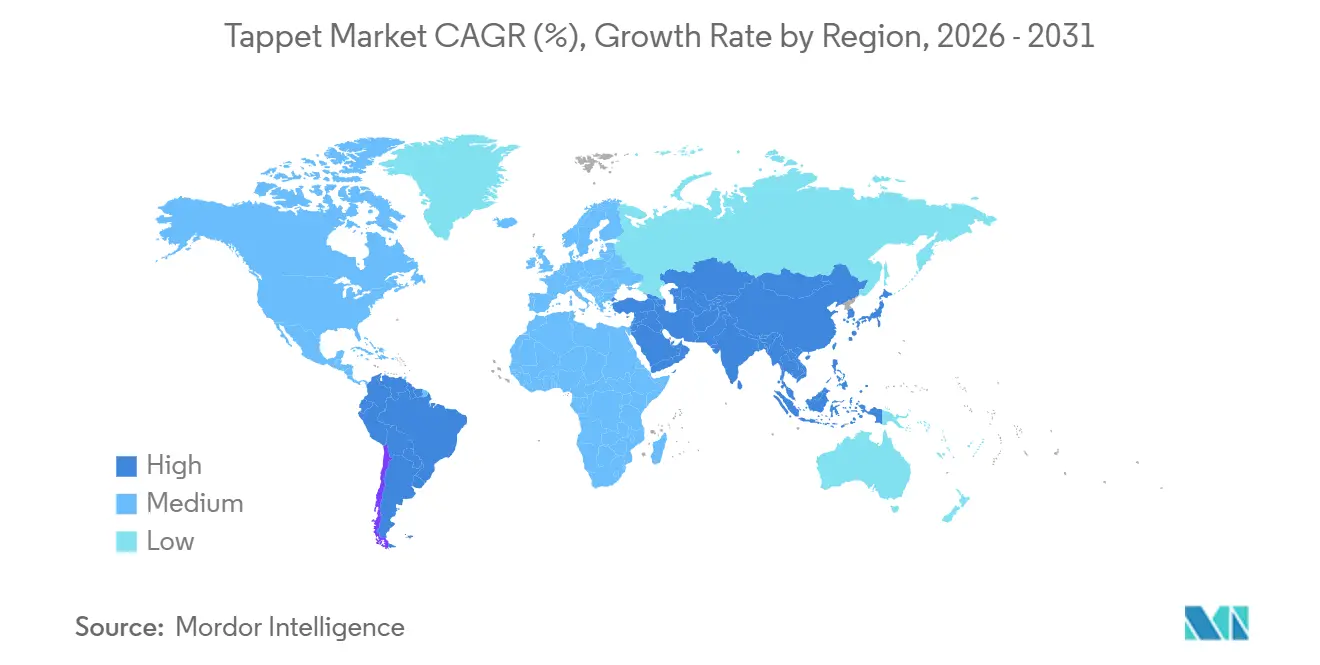

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tappet Market Analysis by Mordor Intelligence

The tappet market size was valued at USD 9.51 billion in 2025 and estimated to grow from USD 9.79 billion in 2026 to reach USD 11.34 billion by 2031, at a CAGR of 2.97% during the forecast period (2026-2031). Asia-Pacific commanded the largest revenue share. Sustained internal-combustion production in India, backed by fresh capital commitments from leading Japanese automakers, offsets the gradual electrification of mature markets. In South America, tariff-free trade on strategic power-train parts agreed in June 2025 is nurturing local assembly operations that keep full valvetrain content intact[1]"Brazil expands automotive trade deal with Argentina," TV BRICS, tvbrics.com . Tightening Euro 7 rules effective in 2027 are steering European and North American manufacturers toward low-friction roller designs that preserve regulatory headroom.

Key Report Takeaways

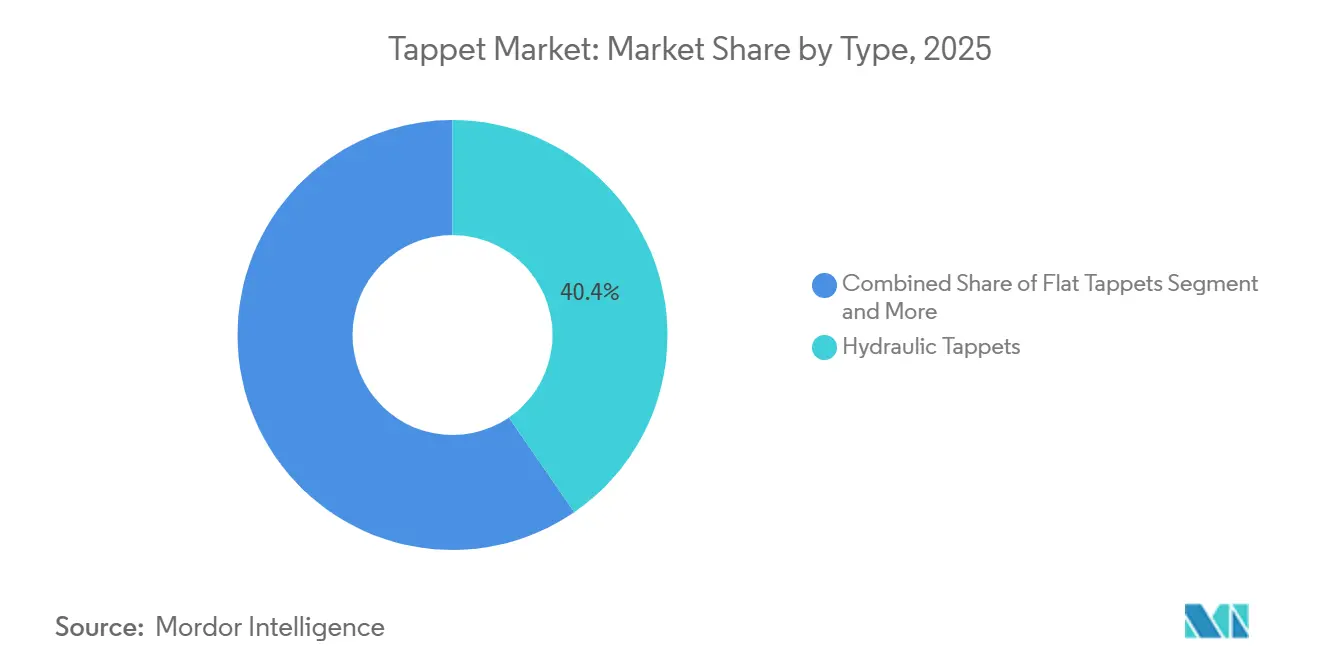

- By type, hydraulic tappets led with 40.43% of the tappet market share in 2025, while roller tappets are projected to expand at a 2.99% CAGR through 2031.

- By engine capacity, the 4-to-6-cylinder segment accounted for 53.32% of the tappet market share in 2025, whereas engines above six cylinders are set to grow at a 3.01% CAGR to 2031.

- By vehicle type, passenger vehicles held 64.05% of the tappet market share in 2025, yet medium- and heavy-duty commercial trucks are forecast to grow at a 5.36% CAGR over the forecast period.

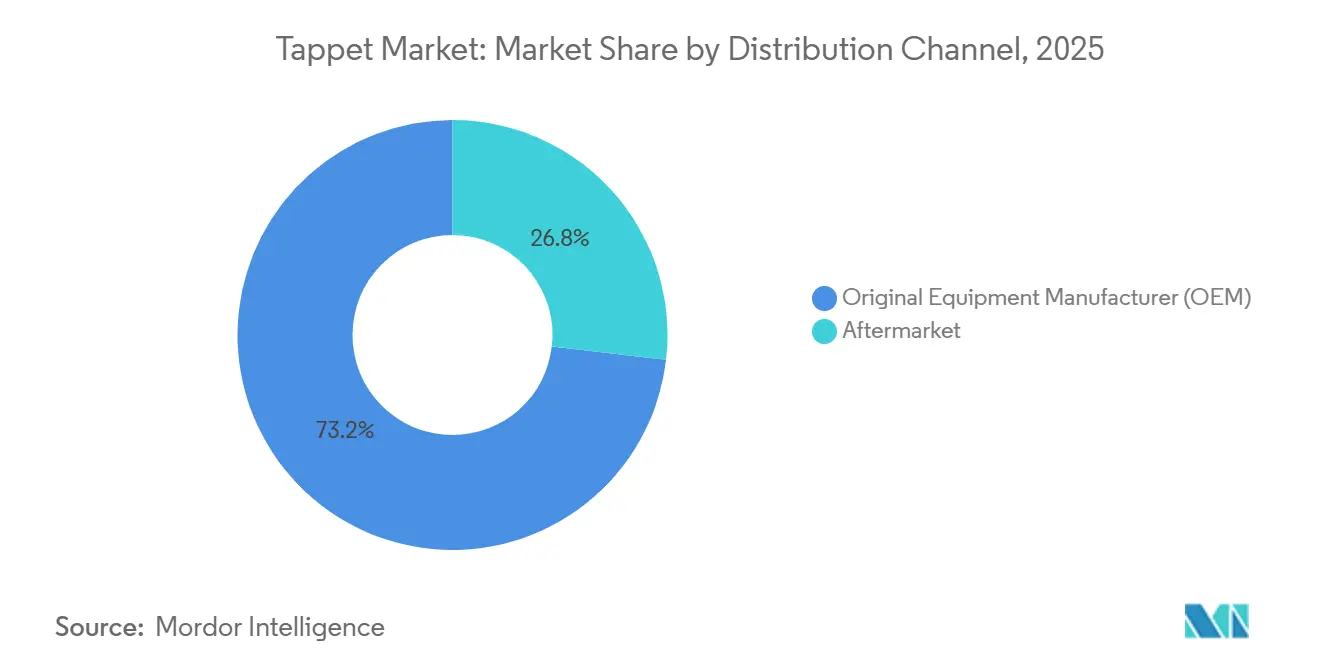

- By distribution channel, OEM sales accounted for 73.16% of the tappet market share in 2025, while the aftermarket is on track for a 3.98% CAGR during the forecast period.

- By fuel type, gasoline engines captured 60.05% of the tappet market share in 2025, but LPG/CNG applications are expected to rise at a 6.31% CAGR to 2031.

- By geography, Asia-Pacific accounted for 47.18% of the Tappet market share in 2025, whereas South America is projected to expand at a 4.13% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tappet Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding ICE Vehicle Production | +0.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Stricter Emission Norms Raise Demand | +0.6% | Global, early gains in Europe and North America | Short term (≤2 years) |

| OEM Shift to Hydraulic Lifters | +0.4% | Global | Long term (≥4 years) |

| Micro-Hybrid Stop-Start Durability Needs | +0.3% | Global | Medium term (2-4 years) |

| Aftermarket Demand for Cam-Train Retrofits | +0.2% | North America and Europe | Short term (≤2 years) |

| Bio-Fuel Compatibility Drives Tappets | +0.1% | Europe, Brazil, India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expanding Production of ICE Vehicles in Asia-Pacific

China’s continued diesel-engine build rates and India’s fresh investment pipeline are sustaining tappet demand despite battery-electric adoption. Japanese exporters are strengthening links with ASEAN plants, securing long-run orders for precision-ground components. Regional suppliers such as Schaeffler India have commissioned new facilities to comply with rising local content requirements. Hybrid penetration keeps full valvetrain architectures in upcoming models, cushioning the market from pure-EV substitution. The result is a stable growth platform that anchors long-term volume in the tappet market.

Stricter Global Emission Norms Heightening Demand for Precision Valvetrain Components

Euro 7 standards taking effect in 2027 mandate tighter real-world compliance, encouraging hydraulic roller followers that hold lash within 0.05 mm tolerances. China’s National VI-b rules have already accelerated the adoption of roller designs in small turbocharged engines. U.S. fleet-average targets are likewise steering engineers toward low-friction tappets to unlock incremental fuel savings. These norms elevate the component from a commodity to a calibrated subsystem. Suppliers able to document precision across temperature swings gain a clear pricing premium.

Growing OEM Shift from Mechanical to Hydraulic/Roller Tappets

Warranty data linking flat-tappet lash drift to misfire and fuel-efficiency penalties is speeding the migration toward self-adjusting hydraulic units. Major platforms such as Cummins’ next-generation X15 rely on roller followers to reach extended service intervals up to 500,000 miles[2]"X15 Efficiency Series (2024)", Cummins Inc., www.cummins.com. Pairing rollers with diamond-like carbon coatings further lowers friction and wear, reinforcing the transition path. The shift reduces maintenance costs for fleet owners and improves cold-start emissions, adding multi-faceted value that supports steady uptake.

Micro-Hybrid Stop-Start Durability Requirements

Stop-start systems impose rapid oil-pressure transients that can collapse older hydraulic lifters, leading to early failures. Tier-one suppliers have responded with check-valve designs rated for 500,000 cycles, triple the prior benchmark. New coatings halve break-in wear to protect during lubrication-starved restarts. As European and North American light-vehicle fleets exceed 70% stop-start penetration, demand for lifters engineered for intermittent duty rises. This design imperative sustains a premium niche within the broader tappet market even as overall ICE volumes plateau.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV Market Penetration | -1.2% | Global, early in Europe and China | Medium term (2-4 years) |

| Alloy and Tool-Steel Volatility | -0.4% | Global | Short term (≤2 years) |

| Emerging Electro-Hydraulic Actuation | -0.3% | Europe, North America | Long term (≥4 years) |

| Tool-Steel Supply Chain Disruptions | -0.2% | Global, concentrated in Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of Battery-Electric Vehicles (ICE Displacement)

Battery-electric models continue to compress the total addressable base of internal-combustion powertrains, particularly in China and the European Union, where consumer incentives and regulatory deadlines overlap. Passenger-car segments that once relied on high-volume four-cylinder engines are shifting toward full electrification, removing entire valvetrain assemblies from their bill of materials. Meanwhile, North America is seeing similar momentum as state-level mandates nudge automakers toward zero-emission fleets. Even so, hybrid drivetrains preserve conventional tappets, softening the blow in regions where charging infrastructure remains uneven.

Volatility in Specialty Alloy and Tool-Steel Prices

Sudden swings in alloy surcharges complicate production planning for tappet makers, many of whom operate on tight contractual pricing with original-equipment customers. When tool-steel costs spike, smaller tier-two suppliers face margin erosion first, widening the competitive gap with vertically integrated incumbents. Purchasing departments have responded by dual-sourcing and experimenting with alternative materials, yet validation cycles for critical engine parts limit rapid substitutions. Freight surcharges layered on top of metal premiums add further unpredictability, especially for cross-continental shipments. The cumulative effect is a risk premium that discourages fresh capacity investments just as demand visibility blurs.

Segment Analysis

By Type: Hydraulic Dominance Meets Roller Efficiency

Hydraulic tappets commanded 40.43% of the tappet market share in 2025, reflecting automakers’ preference for self-adjusting lash control that minimizes maintenance needs. Recent design iterations pair hydraulic function with diamond-like carbon coatings to reduce wear during cold starts, helping keep warranty claims in check. Industry conversations reveal that service departments value the quieter operation such designs deliver, which improves perceived vehicle quality. Flat mechanical lifters now occupy niche roles in classic performance rebuilds where simplicity trumps refinement. Component suppliers are therefore prioritizing hydraulic inventory while supporting legacy formats for specialized aftermarket channels.

Roller tappets, projected to grow at a 2.99% CAGR through 2031, gain traction as friction-reduction mandates sharpen. Their needle-bearing interfaces lessen sliding contact, freeing incremental efficiency that helps meet tightening fleet targets. Engineers also cite lower oil-temperature rise and extended drain intervals as secondary benefits. Adoption accelerates when new engine programs combine overhead cams with direct injection, a pairing that magnifies the payoff from reduced valvetrain losses. As plant tooling amortizes, more mid-cycle refreshes switch to roller profiles, creating a steady conversion pipeline across vehicle classes.

Note: Segment shares of all individual segments available upon report purchase

By Engine Capacity: Mid-Range Cylinders Anchor Demand, Heavy-Duty Blocks Advance

Powerplants with 4-to-6 cylinders accounted for 53.32% of the tappet market share in 2025, largely because this configuration underpins global best-selling models in the passenger and light-commercial segments. Design teams favor a balance between displacement and fuel economy, which translates into long production cycles and stable parts procurement. Aftermarket catalogs mirror this dominance, stocking a broad mix of hydraulic and roller formats tailored to regional fuel qualities. Training programs for independent repair shops therefore focus their curricula around these mainstream engines, reinforcing installed-base advantages. Suppliers in emerging economies often start with mid-range lifter lines before expanding into other capacities.

Engines with more than 6 cylinders are expected to post a 3.01% CAGR, driven by medium- and heavy-duty trucks that continue to use diesel or natural gas combustion. Fleet operators depend on proven longevity, making them receptive to premium roller lifters with advanced coatings that withstand extended service intervals. Regulations on particulate matter continue to tighten, yet high-torque freight requirements leave few realistic electrification alternatives over long distances. Ongoing investments in alternative fuels, such as hydrogen-ready engines, may further increase lifter complexity without reducing overall counts.

By Vehicle Type: Passenger Cars Lead, Commercial Fleets Accelerate

Passenger vehicles held 64.05% of the tappet market share in 2025, benefiting from the sheer scale of global light-vehicle production. Carmakers continue to roll out hybrid variants that retain full mechanical valvetrains, mitigating the effect of battery-only nameplates. Consumer expectations for quiet cabins and low scheduled maintenance keep hydraulic designs in favor, especially in urban markets. Product planners also bundle upgraded lifters with feature packages that tout improved refinement, making valvetrain technology a subtle marketing lever. Consequently, passenger cars remain the benchmark volume driver even as their share edges lower each model year.

Medium and heavy commercial vehicles are on track for a 5.36% CAGR, reflecting freight operators’ cautious but sustained reliance on combustion engines. Long-haul duty cycles demand durable lifters that survive high loads and extended idling without lash drift. Fleet managers, sensitive to downtime, often specify premium roller followers in purchase contracts despite higher acquisition costs. Regulation pushes for cleaner exhaust, yet retrofit options tend to add aftertreatment rather than replace the core engine architecture, preserving tappet requirements. As cross-border trade rebounds, truck production forecasts signal a solid pipeline of new builds that carry full valvetrain content.

By Distribution Channel: OEM Contracts Dominate, Aftermarket Builds Momentum

Original-equipment contracts represented 73.16% of the tappet market share in 2025, locking in predictable volumes tied to vehicle assembly schedules. Tier-one suppliers negotiate multi-year agreements that bundle lifters with complementary valve-train parts, cementing platform loyalty. Production plants emphasize just-in-time sequencing, pushing lifter makers to align logistics systems with final-assembly takt times. Engineering change requests can introduce mid-cycle upgrades, yet contractual frameworks usually safeguard baseline volumes. The OEM channel, therefore, provides the revenue foundation upon which long-term capacity investments rest.

Aftermarket demand is forecasted to expand at a 3.98% CAGR, propelled by lifter replacements following stop-start durability issues and performance-oriented retrofits. Independent garages and enthusiast builders seek drop-in solutions that solve known failure modes without major disassembly. Marketing campaigns highlight coating technologies and improved oiling paths, tapping into consumer anxieties over premature lifter collapse. Online retail platforms broaden reach, allowing niche brands to penetrate regions once dominated by dealership parts counters. This ecosystem fuels steady growth that runs counter-cyclical to new-vehicle sales, offering a hedge for suppliers.

By Fuel Type: Gasoline Retains Scale, LPG/CNG Charts Fastest Lane

Gasoline engines captured 60.05% of the tappet market share in 2025, sustaining their lead through the ubiquity of spark-ignition vehicles worldwide. Even as electrification gains ground, a vast installed base continues to require replacement lifters during overhaul or high-mileage maintenance. Automakers favor hydraulic followers to silence the ticking noises common in older pushrod layouts, thereby enhancing perceived cabin quality. Regulatory tweaks aimed at ethanol blending have nudged material upgrades but have not drastically altered lifter counts.

LPG and CNG applications are projected to rise at a 6.31% CAGR, spurred by favorable fuel-price differentials and urban emissions policies. Engine builders must specify hardened lifters to cope with the drier combustion environment that accompanies gaseous fuels. Fleets appreciate the operating-cost savings, creating a feedback loop that accelerates new-vehicle orders in regions with mature refueling infrastructure. Material scientists respond by developing surface treatments that resist valve-seat recession, a common wear mode in CNG service. As governmental incentives persist, suppliers expect this sub-segment to outpace all others, albeit from a smaller base.

Geography Analysis

Asia-Pacific retained the largest share of tappet demand at 47.18% in 2025, supported by steady internal-combustion vehicle output and widening hybrid penetration. Regional suppliers benefit from vertically integrated casting and heat-treatment lines that shorten lead times for local automakers. Policy frameworks encourage content localization, prompting fresh capacity additions across India, Thailand, and Vietnam. Component exports from Japan into the broader ASEAN bloc continue to rise as manufacturers seek tariff-free corridors inside the Regional Comprehensive Economic Partnership.

South America is forecast to post the fastest regional growth at a 4.13% CAGR through 2031, buoyed by the June 2025 Brazil-Argentina automotive accord, which removed tariffs on strategic powertrain parts. The agreement obliges vehicle assemblers to reinvest in local research facilities, channeling engineering budgets toward materials and coatings suited to high-ethanol blends. Flex-fuel technology dominates the Brazilian passenger-car fleet, driving steady demand for hardened tappets that withstand corrosive exhaust chemistry. Argentina’s truck makers leverage the tariff reprieve to source valvetrain components regionally rather than import from Europe, adding resilience to local supply chains.

North America and Europe continue to generate significant volume even as electrification accelerates. Hybrid and range-extended platforms in both regions still rely on conventional cam-driven architectures, safeguarding baseline lifter consumption. Tightening Euro 7 legislation compels European OEMs to adopt precision roller designs that meet real-world emissions limits. At the same time, U.S. commercial fleets favor durability-oriented lifters specified for long-haul diesel engines. Meanwhile, material-price volatility has prompted many Tier 1 suppliers to expand domestic machining capacity, insulating programs from the effects of geopolitical steel shortages. Collectively, these factors sustain demand in mature markets even as the share of battery-electric vehicles edges upward.

Competitive Landscape

The tappet market exhibits moderate concentration, with long-established suppliers such as Schaeffler, Eaton, Federal-Mogul, Delphi, and MAHLE holding entrenched relationships with global automakers. These incumbents differentiate through surface-treatment know-how, in-house metallurgy, and synchronized global logistics networks that match original-equipment takt times. Asian specialists like Riken and Otics compete aggressively on cost by pairing automated casting lines with captive heat treatment, a combination that shrinks manufacturing cycle time without compromising hardness targets. Collaborative engineering programs between Western OEMs and regional parts makers are becoming common as platforms seek dual sourcing to mitigate risk.

Strategic moves increasingly revolve around hybrid-ready valvetrain technologies. Eaton’s supply agreement for an electromechanical valve-actuation system with Great Wall Motor underscores rising interest in cam-phasing mechanisms that retain hydraulic lash adjustment while adding electric finesse. Schaeffler’s investment in India positions the firm to export roller followers throughout Southeast Asia, sidestepping import duties and shortening time-to-line for regional OEMs. MAHLE, meanwhile, is leveraging hydrogen-combustion truck programs to demonstrate next-generation lifters capable of operating in high-temperature, low-lubricity environments.

Aftermarket-focused brands cultivate niches the OEM channel overlooks. COMP Cams and Hamilton Cams, for instance, address known durability gaps in legacy V8 engines by offering drop-in roller conversions with advanced coatings. Online distribution allows such specialists to reach global enthusiast communities, bypassing traditional dealership parts counters. Performance tuners especially value self-adjusting hydraulic designs that curb valve-train noise at idle yet remain stable above 6,500 rpm. This customer segment prizes incremental refinements over wholesale architectural change, granting profitable islands of demand even as mainstream volumes face electrification pressure.

Tappet Industry Leaders

-

Schaeffler Group

-

Eaton Corporation

-

Federal-Mogul (Tenneco Inc.)

-

Delphi Technologies

-

MAHLE GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Elgin Industries extended its PRO-STOCK line with diamond-like-carbon-coated flat-tappet lifters for classic U.S. V8 engines.

- March 2025: Dumarey completed the takeover of MAHLE Powertrain LLC, adding cylinder-head test cells and prototype roller-lifter lines.

Global Tappet Market Report Scope

The Automotive Tappet market is analyzed across type, engine capacity, vehicle type, distribution channel, fuel type, and geography.

By Type, the market is segmented into Flat Tappets, Roller Tappets, Mechanical Tappets, Hydraulic Tappets, and Pneumatic Tappets. By Engine Capacity, the market is segmented into Below 4 Cylinders, 4-6 Cylinders, and Above 6 Cylinders. By Vehicle Type, the market is segmented into Passenger Vehicles, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles. By Distribution Channel, the market is segmented into OEM and Aftermarket. By Fuel Type, the market is segmented into Gasoline, Diesel, and LPG/CNG. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (United Kingdom, Germany, Spain, Italy, France, Russia, and Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, Egypt, South Africa, and Rest of Middle East and Africa).

Market forecasts are provided in terms of Value (USD).

| Flat Tappets |

| Roller Tappets |

| Mechanical Tappets |

| Hydraulic Tappets |

| Pneumatic Tappets |

| Below 4 Cylinders |

| 4-6 Cylinders |

| Above 6 Cylinders |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| Gasoline |

| Diesel |

| LPG/CNG |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Flat Tappets | |

| Roller Tappets | ||

| Mechanical Tappets | ||

| Hydraulic Tappets | ||

| Pneumatic Tappets | ||

| By Engine Capacity | Below 4 Cylinders | |

| 4-6 Cylinders | ||

| Above 6 Cylinders | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| LPG/CNG | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the tappet market in 2026 and where is it heading?

The tappet market stood at USD 9.79 billion in 2026 and is projected to reach USD 11.34 billion by 2031, registering a 2.97% CAGR.

Which region contributes the highest share of tappet demand?

Asia-Pacific holds the leading position with 47.18% of global revenue, driven by sustained engine production and rapid hybrid adoption.

What is the fastest-growing regional market for tappets?

South America is forecast to grow the quickest at a 4.13% CAGR, supported by tariff-free trade on power-train parts and flex-fuel vehicle proliferation.

Which tappet type shows the quickest adoption rate?

Roller tappets exhibit the fastest uptake, expanding at a 2.99% CAGR as automakers pursue lower friction and tighter emissions compliance.